An estate freeze is not permanent. A wasting freeze gradually unwinds your tax exposure during retirement, a gel preserves your flexibility, a thaw reverses the freeze entirely, and a refreeze resets it at a new value. The right variation depends on where you are today.

One of the most common misconceptions about estate freezes is that they are permanent. In reality, a well-designed freeze is flexible. Your circumstances will change over the years — your business may grow faster or slower than expected, your retirement needs may shift, or your family situation may evolve. The good news is that there are tools to adapt.

In an estate freeze, the business owner (the "freezor") exchanges their common shares for fixed-value preferred shares, locking in the current value. New common shares — worth only a nominal amount — are issued to the next generation or a family trust. All future growth accrues to the new common shares. But what happens after the freeze is implemented depends on which variation you choose and how your circumstances evolve.

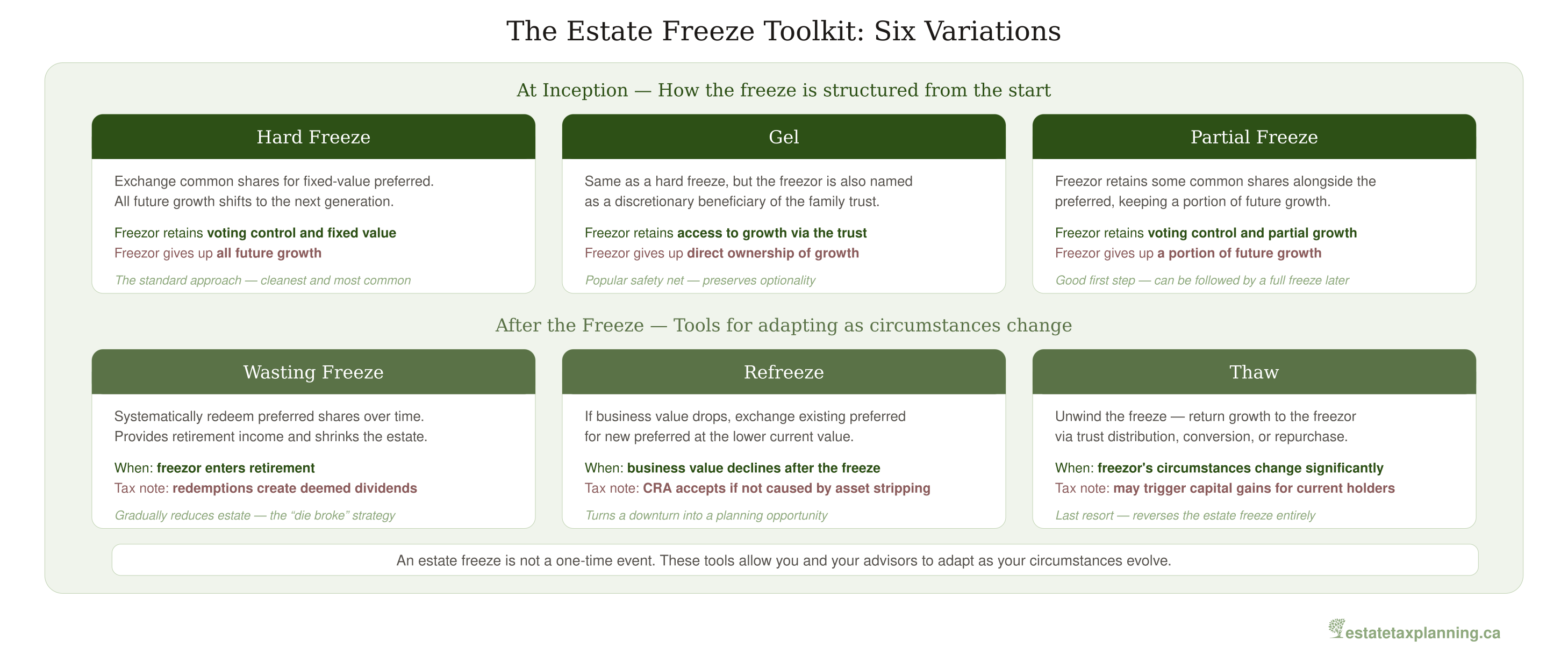

This article brings together the six main variations of the estate freeze — the hard freeze, the gel, the partial freeze, the wasting freeze, the thaw, and the refreeze — plus the related concept of the melt. Understanding these tools gives you and your advisors a full toolkit for managing your freeze over time.

The Estate Freeze Toolkit: Six Variations

The Hard Freeze

A hard freeze is the standard estate freeze. You exchange your common shares for fixed-value preferred shares and walk away from any future growth. All future appreciation accrues to the new common shareholders — your successors or a family trust.

This is the cleanest and most tax-efficient approach, but it requires confidence that you will not need access to the future growth of the business to fund your retirement or other needs. The freezor retains voting control through the preferred shares and can serve as a trustee if a family trust is used, but the economic interest in future growth is gone.

The Gel: A Freeze with a Safety Net

A gel is a modified freeze where the freezor remains a discretionary beneficiary of the family trust that holds the growth shares. This means that while the freeze is implemented in the same way as a hard freeze, the freezor has not completely given up access to future growth. If circumstances change — for example, if retirement savings prove insufficient — the trustees can distribute some of the growth back to the freezor.

The gel is particularly popular with business owners who are in their 50s or early 60s and are not yet certain about their retirement needs. It provides the tax benefits of a freeze while preserving optionality. Inflation can erode the real value of frozen preferred shares over time, which is one reason many freezors choose a gel rather than walking away from growth entirely.

- Provides the tax benefits of a freeze while preserving optionality to access growth if needed.

- Popular with business owners in their 50s and 60s who are uncertain about retirement needs.

- Helps offset inflation erosion on frozen preferred shares.

- Requires careful legal documentation of discretionary distribution rights.

Trade-off — creditor exposure: If the freezor is a beneficiary of the trust, the trust property may in certain circumstances be considered accessible to the freezor's creditors or form part of their estate for family law purposes. This risk needs to be carefully evaluated with legal counsel when structuring the gel.

The Partial Freeze

A partial freeze is a variation where the freezor does not freeze 100% of their interest. Instead, the freezor retains some common shares alongside the new preferred shares, continuing to participate in a portion of the future growth while shifting the rest to the next generation.

For example, if a company is worth $5 million, the freezor might freeze $4 million into preferred shares and retain common shares representing 20% of the future growth. This gives the freezor ongoing participation in the business's success while still shifting 80% of the future growth to the next generation.

When it makes sense: A partial freeze is useful when the freezor wants some continued upside, when the freezor wants to demonstrate to the next generation that they still have "skin in the game," or when the succession plan calls for the freezor to gradually reduce their common shareholding over time through subsequent refreezes.

- Requires two share classes with different economic rights.

- The frozen preferred class value and the growth common class value must both be independently defensible.

- Tax deferral eligibility and rollover treatment depend on precise valuation of both classes.

- A CBV report should clearly separate the valuation of each class.

One valuation nuance that is often overlooked: the common shares retained by the freezor may carry a minority discount or lack-of-control discount depending on the percentage retained and the rights attached to each share class. Conversely, the preferred shares may carry a premium if they include voting control, redemption rights, or priority on liquidation. These discounts and premiums must be reflected in the valuation — if they are not, the CRA may reassess the freeze transaction and the intended tax deferral could be jeopardized. Your CBV should address these factors explicitly in the valuation report.

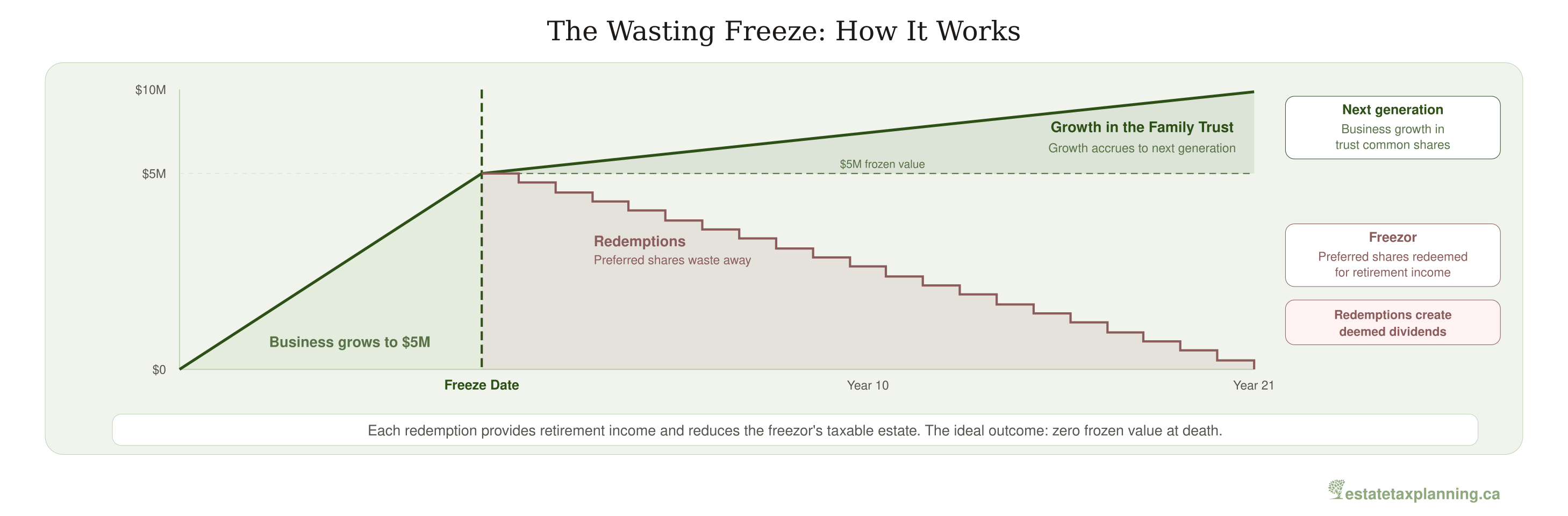

The Wasting Freeze: Gradually Shrinking Your Estate

A wasting freeze combines an estate freeze with a systematic program of redeeming the frozen preferred shares over time. Each year, the corporation redeems a portion of the freezor's preferred shares, paying out their value in cash. This provides retirement income to the freezor while simultaneously reducing the value of their estate.

The wasting freeze achieves several things at once. It provides retirement cash flow through regular redemptions. It reduces the freezor's estate over time, lowering both the capital gains tax at death and probate fees. And it spreads the tax burden over many years, which can keep the freezor in a lower marginal tax bracket compared to a single large disposition at death.

A concrete example: A husband and wife each hold $2.5 million in frozen preferred shares after a freeze. If each redeems $125,000 per year over 20 years, the full $5 million is returned to them as retirement income, and their combined frozen estate is reduced to zero. At a 50% capital gains inclusion rate and approximately 53% combined marginal tax rate, eliminating $5 million in frozen value could save roughly $1.3 million in tax at death.

Capital dividends: a powerful accelerator. If the corporation has a balance in its Capital Dividend Account (CDA) — for example, from the non-taxable portion of capital gains realized corporately or from life insurance proceeds — capital dividends can be paid to the freezor tax-free. Strategically allocating capital dividends as part of the annual redemption schedule can significantly reduce the tax cost of the wasting freeze, effectively turbo-charging the estate reduction strategy. Your tax advisor should model the optimal mix of eligible dividends, capital dividends, and share redemptions each year.

- Redemptions provide systematic retirement cash flow — for many of our clients, this becomes their largest single income source in retirement.

- Spreads tax liability over many years, potentially keeping the freezor in lower marginal brackets.

- Capital dividends can be allocated tax-free as part of the redemption schedule. We always check the CDA balance first.

- The estate is progressively reduced, lowering probate fees and death tax liability. In Ontario, this alone can save tens of thousands of dollars.

The melt: a related concept. A melt is broader than a wasting freeze. It refers to any method of diverting appreciation back to the freezor without modifying the corporate structure — including increasing dividends on the preferred shares, raising the freezor's salary or management fees, or gradually redeeming shares. The wasting freeze is a specific type of melt focused on systematic share redemption.

Post-Freeze Dividend Policy: Dividends vs. Redemptions

Once the freeze is in place, the freezor needs ongoing income — typically from the corporation that holds their preferred shares. The two main sources are dividends declared on the preferred shares and periodic share redemptions (the wasting freeze). Each has different tax consequences, and the optimal mix depends on the corporation’s surplus accounts, the freezor’s personal tax situation, and the family’s TOSI exposure.

Dividends on Preferred Shares

Eligible vs. non-eligible dividends. If the corporation has a GRIP balance (income taxed at the general corporate rate), it can pay eligible dividends, which receive a more favourable gross-up and dividend tax credit at the personal level. If the corporation’s income was taxed at the small business rate, dividends are non-eligible and carry a higher personal tax cost. Your tax advisor should model both scenarios annually to determine the most tax-efficient dividend type.

Capital dividends from the CDA. If the corporation has a capital dividend account balance — from the non-taxable portion of capital gains, life insurance proceeds, or capital dividends received from other corporations — it can pay capital dividends to the freezor entirely tax-free. Capital dividends should generally be paid first, before eligible or non-eligible dividends, because they have zero personal tax cost. However, the CDA election (under subsection 83(2)) must be filed before or at the time the dividend is paid, and an overstatement of the CDA balance triggers a Part III tax of 60% on the excess.

Dividends to family members and TOSI. If the family trust or individual family members hold growth shares, dividends on those shares may be subject to the tax on split income unless a TOSI exception applies. The excluded business exception requires regular, continuous, and substantial involvement (approximately 20 hours per week). The excluded shares exception requires direct ownership of at least 10% of votes and FMV. Dividends paid to family members who do not qualify for an exception are taxed at the top marginal rate regardless of the recipient’s actual income.

Redemptions vs. Dividends: When to Use Each

Redemptions create deemed dividends. When preferred shares are redeemed, the excess of the redemption amount over the paid-up capital is treated as a deemed dividend under subsection 84(3). Since PUC in a standard freeze is typically nominal, almost the entire redemption amount is a deemed dividend. The character of the deemed dividend (eligible or non-eligible) depends on the corporation’s GRIP and LRIP balances.

When dividends are better. Paying dividends on preferred shares (without redeeming) keeps the freeze value intact for longer, which may be desirable if the freezor wants to preserve the full redemption value as a safety net. Dividends also avoid the administrative complexity of partial redemptions (board resolution, share certificate cancellation, PUC tracking).

When redemptions are better. Redemptions permanently reduce the freezor’s estate. Every dollar redeemed is a dollar that will not be subject to the deemed disposition at death. For a freezor who has sufficient retirement income and wants to minimize the estate’s tax liability, systematic redemptions are more powerful than dividends because they shrink the estate.

- Model the corporation’s after-tax free cash flow before committing to a redemption schedule. The corporation must be able to fund the redemptions without starving the operating business of capital.

- Consider the impact on the passive income grind — investment income from reinvested redemption proceeds in the freezor’s hands may push the corporate group’s AAII above $50,000, reducing the small business deduction.

- Coordinate with the freezor’s OAS, CPP, and RRIF income. Deemed dividends from redemptions increase the freezor’s net income, potentially triggering the OAS clawback (approximately $93,454 threshold for 2026, indexed annually).

- Stress-test the plan: if revenue drops 20–30%, can the corporation still meet the redemption schedule? Build in flexibility to pause or reduce redemptions in lean years.

- Review the CDA balance and pay capital dividends first (tax-free). If a capital dividend accidentally exceeds the CDA balance, the subsection 184(3) corrective election may allow the excess to be reclassified as a taxable dividend rather than triggering Part III tax — see Life Insurance and the Estate Freeze for the full CDA mechanics.

- Check the GRIP balance to determine if eligible dividends are available.

- Model the freezor’s total income to avoid OAS clawback.

- Assess TOSI exposure for any dividends to family members on growth shares.

- Compare the tax cost of a dividend versus a share redemption at the current marginal rate.

- Confirm life insurance coverage still matches the remaining freeze value after any redemptions.

The Thaw: Reversing the Freeze

A thaw is the process of unwinding an estate freeze, returning the growth to the original freezor. This is typically done when the freezor's circumstances have changed significantly — for example, if they need more assets than their frozen shares provide, or if the planned succession has fallen apart.

Consider this example: David froze at age 52, expecting his daughter to take over the business. Five years later, she left to pursue a different career. With no successor in place and insufficient retirement savings outside the frozen shares, David's advisor recommended a partial thaw — converting a portion of the trust's growth shares back to David — to restore his access to the appreciation that had accrued since the freeze. Without the thaw, David's retirement security depended entirely on the fixed redemption value of his preferred shares, which inflation had been quietly eroding.

There are several ways to implement a thaw. If the freeze used a gel structure, the trustees can distribute the growth shares from the trust to the freezor, generally on a tax-deferred basis under subsection 107(2). If the preferred shares include a conversion privilege, the freezor may be able to convert them back into common shares on a tax-deferred basis. Or the freezor can acquire the common shares from the current holders, though this may trigger an immediate capital gain for the sellers — potentially offset by the LCGE if the shares qualify as QSBC shares.

- All thaw methods have potential tax implications and require professional guidance.

- A thaw is generally a last resort when the freeze no longer serves the freezor's objectives.

- Distributing growth shares from a trust may trigger capital gains in the trust if subsection 107(2) rollover conditions are not met.

- Acquiring common shares back from successors could trigger unwanted capital gains for them.

- If a family trust was used, the thaw must be completed before the 21-year deemed disposition — otherwise the trust faces a taxable event on the accrued gains.

A thaw should never be attempted without the guidance of a qualified tax advisor. It is a last resort, used when the freeze no longer serves the freezor's objectives. Even so, having the ability to unwind the freeze is one of the reasons many advisors recommend building flexibility into the freeze structure from the start — through retractable and convertible share provisions, and through a gel structure that keeps the freezor as a discretionary beneficiary.

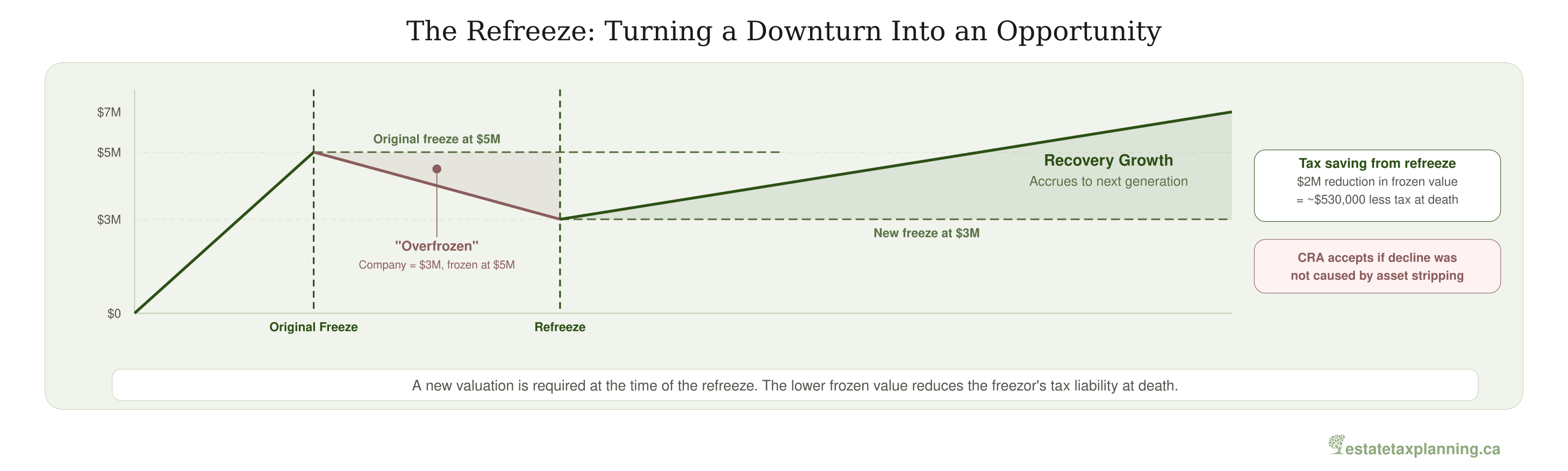

The Refreeze: Turning a Downturn Into an Opportunity

A refreeze is implemented when the value of the business has declined since the original freeze. The freezor exchanges their existing preferred shares (frozen at the original, higher value) for new preferred shares frozen at the current, lower fair market value. New common shares are issued to capture the future recovery.

Consider this scenario: You implemented a freeze when your company was worth $5 million. Two years later, an economic downturn has reduced the value to $3 million. Your preferred shares are still worth $5 million on paper, but the company's actual value is only $3 million. You are "overfrozen."

By refreezing at $3 million, you reduce your frozen value by $2 million. At a 50% capital gains inclusion rate and a combined marginal rate of approximately 53%, that is roughly $530,000 less tax at death. When the company recovers to $5 million and beyond, that recovery growth belongs to the next generation rather than being caught in your frozen interest.

- Appropriate when business value has declined materially since original freeze.

- Reduces frozen value and corresponding death tax liability.

- Requires a new independent valuation by a CBV at the time of the refreeze.

- Future recovery from the refreeze value goes to next generation.

- CRA generally accepts refreezes where the decline is due to genuine business factors, not deliberate asset stripping.

- The CRA may challenge a refreeze if the decline in value was caused by deliberate asset stripping or non-arm's length transactions designed to reduce the freeze value artificially.

- Maintain contemporaneous documentation of the business reasons for the decline in value.

- The new valuation must be independent and defensible — a CBV report is essential.

- If the refreeze uses section 86 (share exchange), ensure all the technical requirements of that provision are met to preserve tax deferral.

Putting It All Together

An estate freeze is not a one-time event — it’s the beginning of an ongoing planning process. The flexibility to gel, thaw, waste, or refreeze gives you tools to adapt as your life, your business, and the tax environment evolve. The families who get the most value from their freeze are the ones who review it annually and ask a simple question: has anything changed that warrants an adjustment? If the answer is yes, the tools in this article give you a way to respond.

Now that you understand the full toolkit for adapting an estate freeze, the next important consideration is how income splitting rules affect your freeze. In TOSI and the Estate Freeze , we examine the tax on split income rules and how they determine whether dividends paid to family members through a freeze structure are taxed at the top marginal rate or at the recipient’s own rate.

For definitions of the key terms used in this article — including estate freeze, gel structure, wasting freeze, thaw, and refreeze — see our Key Terms and Definitions reference guide.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Estate freezes are complex transactions that require the coordinated involvement of qualified tax, valuation, and legal professionals. Always consult your advisors before acting on any of the information discussed here.