The LCGE can shelter up to $1,275,000 per family member in 2026. Multiply it through a family trust, crystallize it at the freeze to step up your cost base, and start purifying the corporation at least 24 months before the freeze date. Model the AMT before crystallizing — the post-2024 rules can produce a surprise tax bill even when the LCGE fully offsets the regular gain.

The Lifetime Capital Gains Exemption (LCGE) is one of the most significant tax planning opportunities available to Canadian business owners. It allows each individual to shelter up to $1,275,000 in capital gains on the disposition of qualified small business corporation (QSBC) shares from tax (indexed to inflation; $1,275,000 for 2026). In the context of an estate freeze, the LCGE can be used in multiple ways to reduce the family’s overall tax burden — sometimes by millions of dollars.

But the LCGE is not automatic. The shares must qualify, the timing must be right, and the interaction with Alternative Minimum Tax must be carefully managed. This article explains how the LCGE works in the estate freeze context, how to multiply it across the family, when and how to crystallize it, and what can go wrong if the planning is not done properly.

What Is the LCGE?

The LCGE is a lifetime exemption that allows Canadian residents to realize capital gains on qualifying shares without paying tax, up to a cumulative limit. The limit was increased to $1,250,000 per individual effective June 25, 2024 (up from approximately $1,016,836), and is indexed to inflation beginning in 2026. For 2026, the indexed limit is $1,275,000.

The exemption applies to capital gains on the disposition of QSBC shares, qualified farm property, and qualified fishing property. In the estate freeze context, we are concerned with QSBC shares — specifically, the preferred shares received by the freezor and the growth shares held by family members or a family trust.

- Canada first introduced a general $100,000 lifetime capital gains exemption in 1985, available on all capital property. That broad exemption was eliminated in 1994, but the QSBC-specific exemption survived and has grown ever since. The QSBC exemption was $500,000 from 2006 to 2014, rose to $800,000 in 2014 (indexed from 2015), and by 2023 had reached approximately $971,190.

- The June 2024 budget increased the limit to $1,250,000 in a single jump — the largest increase in the exemption’s history. Indexation to inflation resumes in 2026.

- For a family of four implementing an estate freeze with LCGE multiplication, the combined shelter has grown from $2 million (2006) to approximately $5.1 million in 2026. Every increase is another reason to structure your freeze to multiply this exemption across family members.

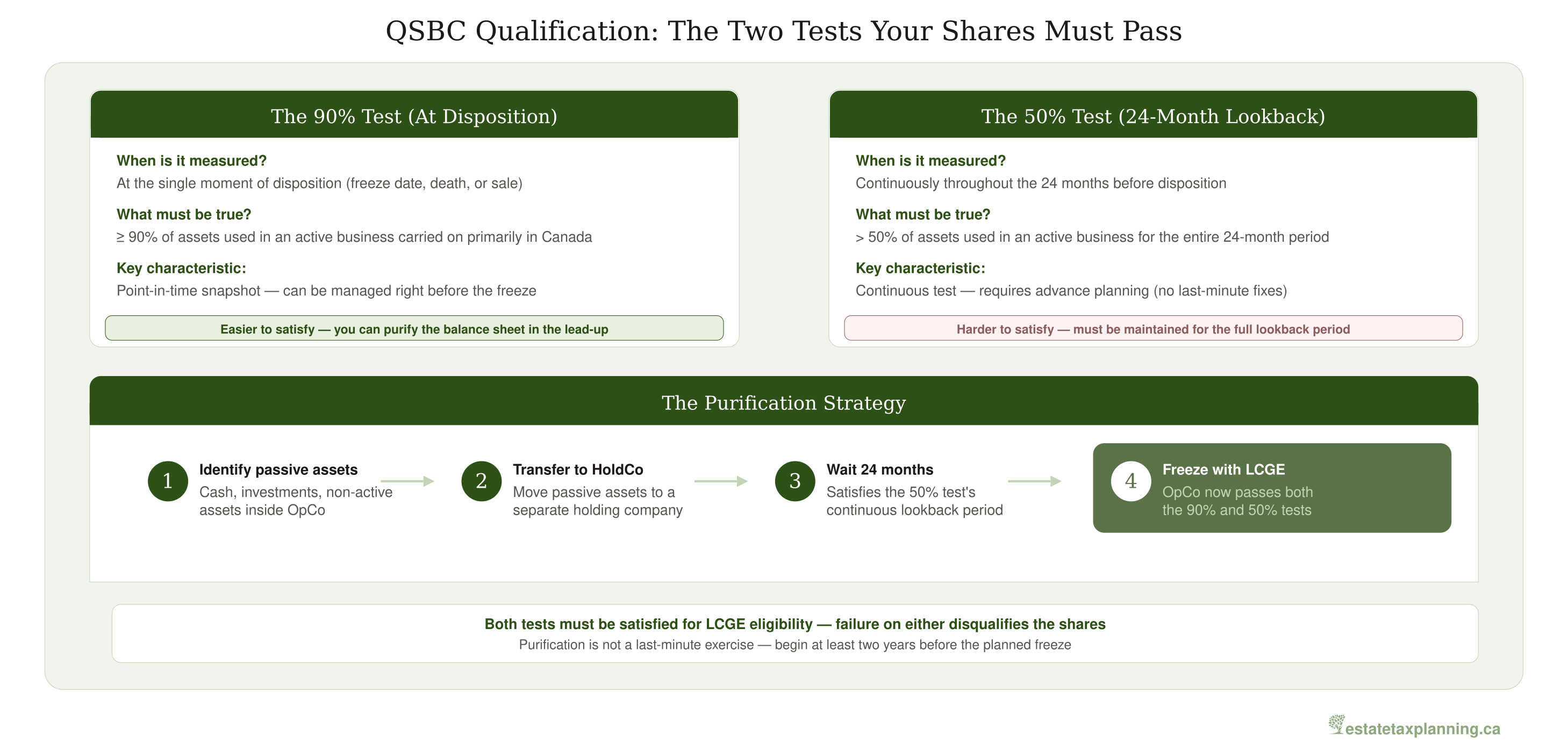

Qualifying for the LCGE: The QSBC Share Tests

For the LCGE to apply, the shares must qualify as QSBC shares at the time of disposition. This requires meeting two asset-based tests, both of which must be satisfied.

The 90% Test

At the time of the disposition (including a deemed disposition at death or a freeze transaction), at least 90% of the corporation’s assets must be used in an active business carried on primarily in Canada. This is measured at a single point in time — which means it can be managed in the lead-up to the freeze.

The 50% Test

Throughout the 24 months preceding the disposition, more than 50% of the corporation’s assets must have been used in an active business. This is a continuous test — it must be met for the entire 24-month period, not just at a single point. This is the harder test to satisfy, because it cannot be fixed at the last minute.

Consider a corporation with $3 million in total assets — $2.5 million in active business equipment and receivables, plus a $500,000 stock portfolio. The corporation fails the 90% test because only 83% of its assets are active. If the stock portfolio is transferred to a holding company before the freeze, the operating company passes the 90% test easily. But the 50% test looks back 24 months: if the stock portfolio was held inside the corporation for 13 of the preceding 24 months, the 50% test may still fail — even though the assets are gone today. This is the critical difference between a point-in-time test and a continuous test.

The Holding Period Requirement

In addition to the asset tests, the shares must have been owned by the taxpayer — or by a person related to the taxpayer — throughout the 24 months immediately preceding the disposition. In the estate freeze context, this is usually straightforward for the freezor, who held the original common shares before exchanging them. However, it can become an issue when shares are held through a family trust and gains are allocated to beneficiaries who were not shareholders during the full 24-month window. The holding period is tested at the shareholder level, and planning must account for it when new beneficiaries are added to the trust or when shares are issued to family members close to a planned disposition.

- One common trap arises when a family trust distributes shares to a beneficiary shortly before a sale. The beneficiary may not have personally owned the shares for 24 months. The holding period can be met through related-party ownership — including ownership by the trust itself — but the rules are nuanced: the beneficiary must be related to the person who owned the shares throughout the relevant period.

- When planning for the 21-year deemed disposition deadline or a potential sale, the timing of share rollouts from the trust to individual beneficiaries must account for this holding period requirement. A distribution that occurs too close to the disposition can disqualify the shares from LCGE eligibility in the beneficiary’s hands, even if the trust held them for decades.

The Purification Strategy

Many successful businesses accumulate surplus cash and passive investments over time. Investment portfolios, excess cash reserves, and other non-active assets can push the corporation below the 90% threshold, disqualifying the shares from LCGE eligibility.

The solution is to “purify” the operating company by transferring passive assets to a separate holding company before the freeze. This raises the ratio of active business assets in the operating company above the 90% threshold.

- Because the 50% test looks back 24 months continuously, purification must begin at least two years before the planned freeze date. This is not a last-minute exercise.

- A business owner who decides in January to freeze in March cannot retroactively fix the asset composition for the prior 24 months. The timeline for LCGE planning often begins well before the freeze itself.

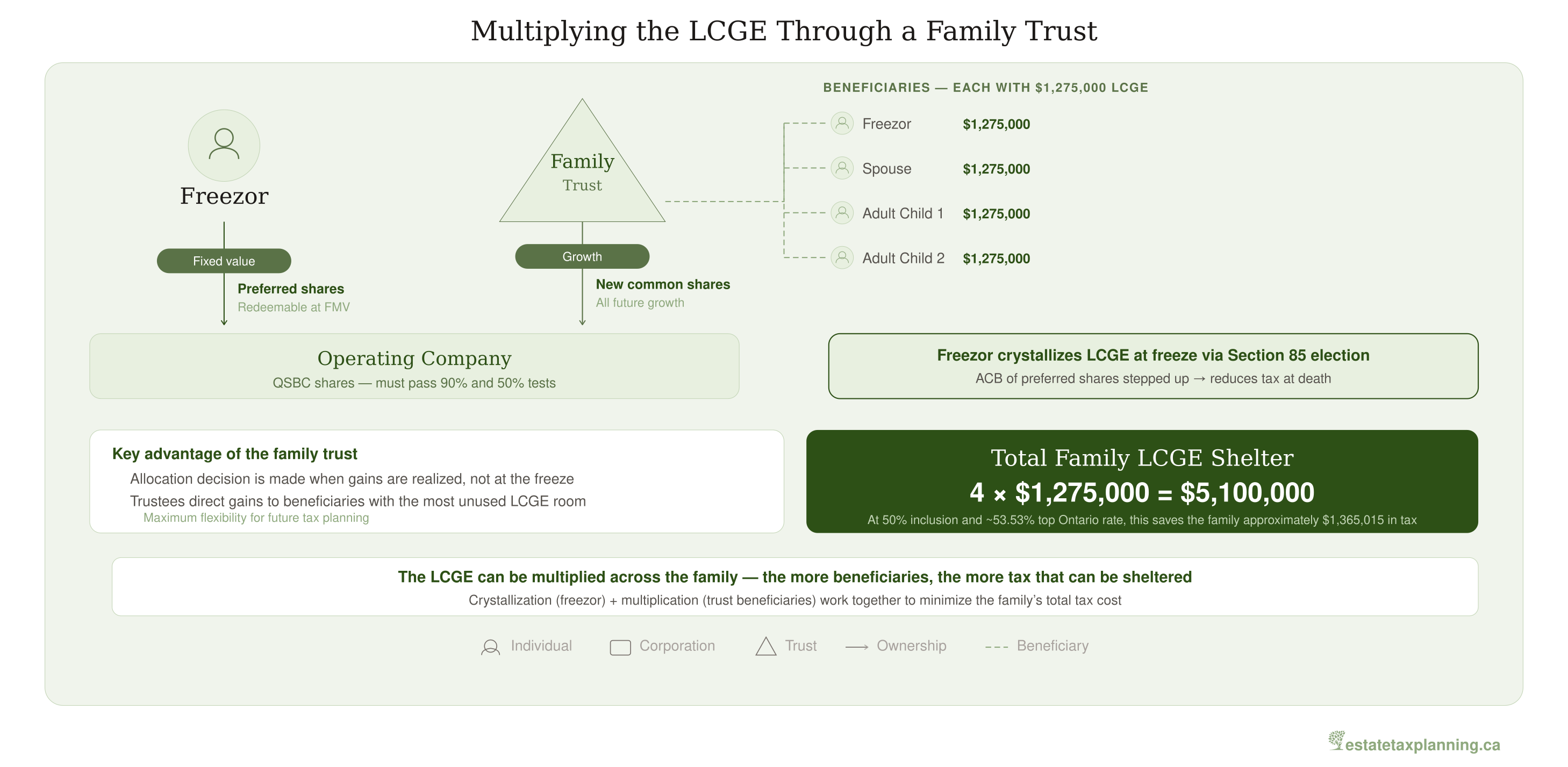

Multiplying the LCGE Across the Family

By involving multiple family members as shareholders — either directly or through a family trust that allocates capital gains to individual beneficiaries — the LCGE can be multiplied across the family. For a family of four (two parents and two adult children), this could shelter up to approximately $5.1 million in capital gains (using the 2026 indexed limit of $1,275,000 per individual).

This is one of the most significant tax planning opportunities available through an estate freeze. A family trust is the most common vehicle for LCGE multiplication. The trust holds the growth shares and, when gains are realized, the trustees allocate the gains to whichever beneficiaries have unused LCGE room.

Worked Example: A Family of Four

The family trust holds growth shares now worth $4 million. On a disposition, the trustees allocate the capital gain equally to four beneficiaries — the freezor, the freezor’s spouse, and two adult children. Each beneficiary’s $1 million share of the gain is fully sheltered by their individual LCGE (each has $1,275,000 in available room). Total tax on the $4 million gain: $0.

Without the trust and LCGE multiplication, the same $4 million gain taxed entirely in the freezor’s hands would produce a taxable capital gain of $2 million (at the 50% inclusion rate), generating approximately $1.07 million in combined federal and Ontario tax at the top marginal rate. The LCGE multiplication strategy saves the family over $1 million in tax on this single transaction — and the savings grow as the business grows.

- The allocation decision is made at the time the gains are realized, not at the time the freeze is implemented. This is one of the biggest advantages of the trust structure.

- The trustees can direct gains to whichever family members have the most unused LCGE room, adapting to circumstances that may have changed since the freeze was first put in place. We’ve seen families where the original plan shifted completely over fifteen years — the trust gave them the flexibility to adjust.

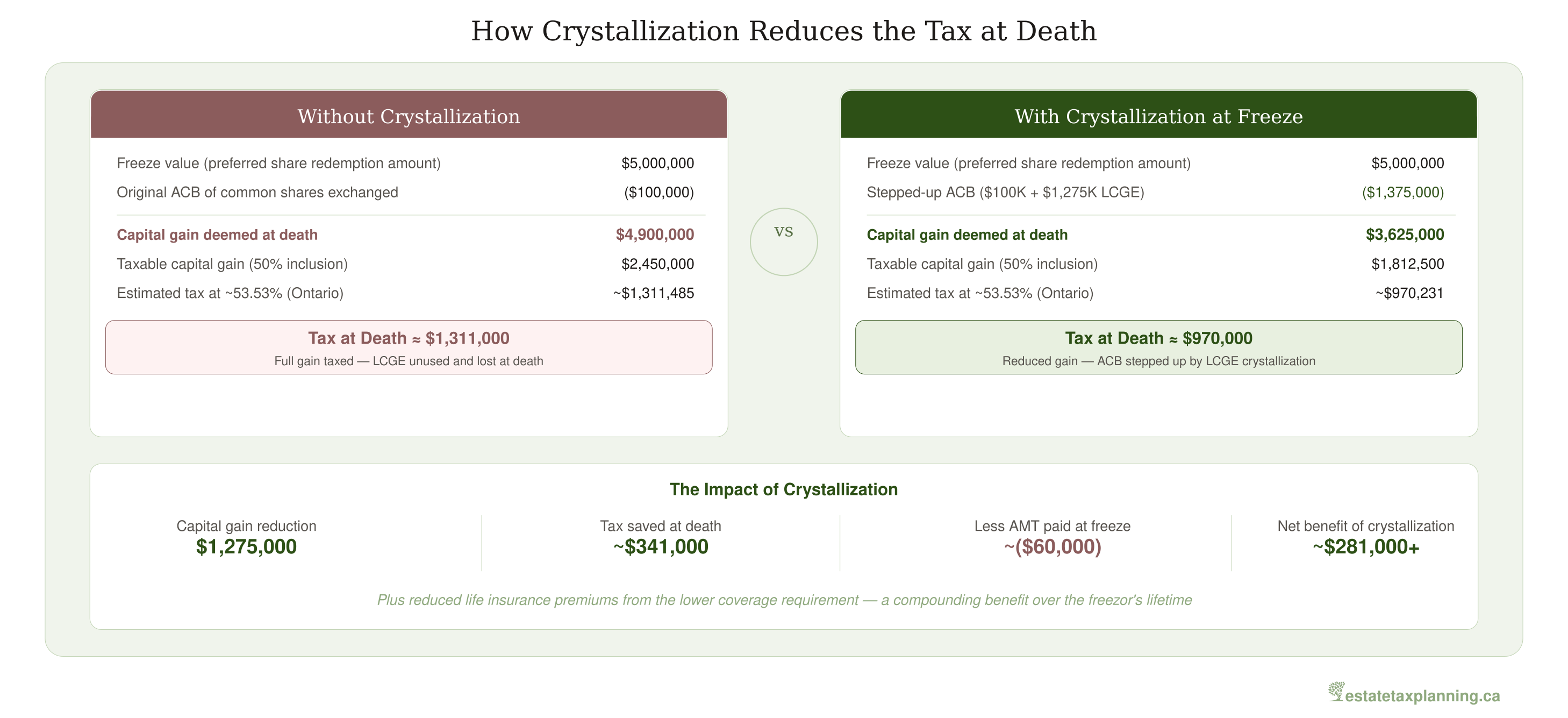

Crystallizing the LCGE

At the time of the estate freeze, the freezor may choose to “crystallize” their LCGE by electing a transfer amount under subsection 85(1) that triggers a capital gain equal to the available exemption. The LCGE deduction offsets the gain, and the preferred shares receive a higher adjusted cost base (ACB) as a result.

This reduces the capital gain that will be triggered at death, effectively using the LCGE today to lower a future tax bill. Crystallizing requires a Section 85 election — it is not available under a Section 86 reorganization. If the freeze is structured as a Section 86 share exchange, a separate step may be needed to achieve crystallization.

- Without crystallization, the freezor’s preferred shares have an ACB equal to the original cost of the shares exchanged. At death, the deemed disposition triggers a gain on the full difference between the redemption value and the ACB.

- By crystallizing, the ACB is stepped up by the amount of the LCGE claimed — reducing the eventual deemed gain dollar for dollar. This also reduces the amount of life insurance coverage needed to fund the tax at death.

- The analysis throughout this article assumes the current 50% capital gains inclusion rate. In 2024, the federal government proposed increasing the inclusion rate to 66.67% for gains above $250,000 — a change that was ultimately cancelled on March 21, 2025. Had it taken effect, the crystallization math would have changed significantly: the taxable portion of a $1,275,000 crystallization would have risen from $637,500 to approximately $934,000 (after the $250,000 threshold), and the AMT interaction would have been even more complex.

- If the inclusion rate were to change in the future, the crystallization calculations, AMT modelling, and insurance coverage estimates in this article would all need to be revisited. This is one reason to work with a qualified tax advisor who can model the current rules at the time of the freeze.

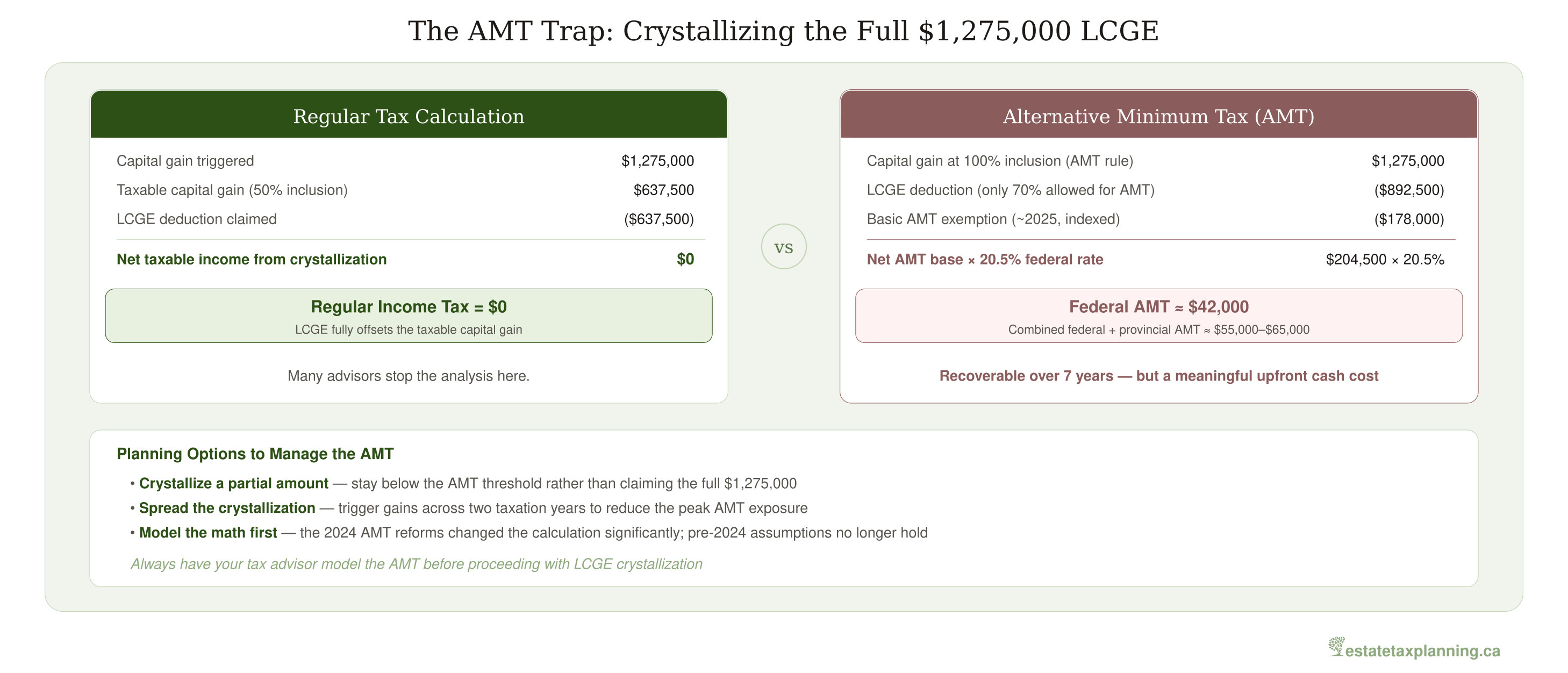

The AMT Trap When Crystallizing

Crystallizing the LCGE eliminates regular income tax on the triggered gain. But it may not eliminate Alternative Minimum Tax. Under the AMT rules that took effect on January 1, 2024, the calculation diverges significantly from the regular tax calculation — and the result can be a substantial unexpected tax bill in the year of the freeze.

Numerical Example

The scenario: A business owner implements a Section 85 freeze and elects to crystallize the full $1,275,000 LCGE. The elected amount triggers a $1,275,000 capital gain, which is fully offset by the LCGE deduction on the regular return. Regular income tax on the crystallization = $0.

The AMT calculation: For AMT purposes, the capital gain is included at 100% ($1,275,000), not the regular 50%. The LCGE deduction is only 70% allowed for AMT purposes ($892,500). After the basic AMT exemption of approximately $173,000 in 2024 ($178,000 in 2025, indexed annually), the remaining AMT base of roughly $204,500 is taxed at the federal AMT rate of 20.5%. Result: approximately $42,000 in federal AMT, plus provincial AMT.

The total AMT hit: Depending on the province, the combined federal and provincial AMT could be approximately $55,000–$65,000 in the year of the freeze. This amount is recoverable over the following seven years by applying it as a credit against regular tax — but only if the taxpayer generates enough regular tax in those years to absorb the credit. It represents a meaningful upfront cash cost that many business owners do not expect.

- The math changed significantly with the 2024 AMT reforms, and pre-2024 planning assumptions no longer hold.

- In some cases, it may be better to crystallize a partial amount rather than the full LCGE, or to spread the crystallization across two taxation years to stay below the AMT threshold. A qualified tax advisor should model the AMT calculation before any crystallization decision is finalized.

What Happened to the Canadian Entrepreneurs’ Incentive?

The Canadian Entrepreneurs’ Incentive (CEI) was proposed in Budget 2024 alongside the capital gains inclusion rate increase. It would have reduced the inclusion rate to one-third on qualifying gains, with a lifetime limit phasing from $400,000 in 2025 to $2 million by 2029. However, the CEI was never enacted into law.

When Prime Minister Carney cancelled the proposed capital gains inclusion rate increase on March 21, 2025, the rationale for the CEI — which was designed to offset the higher inclusion rate for qualifying entrepreneurs — fell away. Budget 2025 (November 4, 2025) confirmed that the CEI has been eliminated. It was never proclaimed in force and no taxpayer was able to claim it.

- The CEI was proposed in Budget 2024 but was never enacted into law. Budget 2025 confirmed its cancellation.

- Do not plan around the CEI. Any references to it in older planning materials should be disregarded.

- The LCGE remains the primary capital gains shelter for QSBC share dispositions. Focus your planning there.

Practical Planning Considerations

Timing the Crystallization

LCGE crystallization is most commonly done at the time of the estate freeze, because that is when the Section 85 election is filed. The key is ensuring the shares qualify as QSBC shares at the time of the election — which brings us back to the 90% and 50% tests discussed above.

Coordination with Insurance

The LCGE directly affects the amount of life insurance coverage needed. By crystallizing the exemption and stepping up the ACB of the preferred shares, the eventual capital gain at death is reduced. This means fewer insurance dollars are required to fund the tax liability — potentially saving the corporation tens of thousands of dollars in premiums over the freezor’s lifetime. For example, if crystallizing the full $1,275,000 LCGE steps up the ACB and reduces the eventual gain by that amount, the tax savings at death could be roughly $341,000 (at the 50% inclusion rate and Ontario’s top combined rate). That translates directly into lower coverage requirements and lower annual premiums for the corporate-owned policy discussed in Life Insurance and the Estate Freeze.

Monitoring QSBC Status Over Time

QSBC qualification is not a one-time event. If the shares are held through a family trust, the QSBC tests must be met at the time the gains are eventually realized — which could be years or decades after the freeze. Changes in the business — adding passive investments, acquiring rental properties, or accumulating excess cash — can cause shares to lose their QSBC status. Ongoing monitoring is essential, particularly as the 21-year trust disposition deadline approaches.

- 24+ months before freeze: Begin purification if needed — transfer passive investments and excess cash to a holding company. The 50% continuous test requires a full 24-month clean window.

- 12 months before freeze: Confirm QSBC status with a CBV or qualified tax advisor. Obtain an independent valuation if the freeze amount is material. Review the 90% and 50% tests with current financial statements.

- At the freeze: File the Section 85 election with the crystallization amount. Model the AMT before finalizing the elected amount. Ensure all family members or trust beneficiaries who will claim the LCGE are Canadian residents.

- Post-freeze: Model AMT recovery over the following 7 years. Monitor whether the freezor generates enough regular tax to absorb the AMT credit. Consider timing of other income sources.

- Ongoing: Monitor QSBC status for trust-held growth shares. Changes in the business — accumulating passive assets, acquiring real estate, or adding investment income — can disqualify shares before the eventual disposition. Review annually as the 21-year deemed disposition deadline approaches.

Making the Most of the LCGE

The LCGE is the most powerful tax shelter available to Canadian business owners selling or transitioning their business. In the estate freeze context, it serves three purposes: it reduces the freezor’s personal tax liability through crystallization, it shelters gains for family members through multiplication, and it lowers the life insurance coverage required to fund the remaining tax.

But it requires planning. QSBC qualification must be established and maintained. Purification may need to begin years in advance. The AMT implications of crystallization must be modeled. And the interaction with the family trust, the wasting freeze, and the insurance strategy must be coordinated.

The stakes are high enough that the planning is worth getting right. A qualified tax advisor can model the AMT, confirm QSBC status, and coordinate the crystallization with the freeze mechanics, while a CBV provides the independent valuation that anchors the elected amount.

What’s Next

Even with careful LCGE, TOSI, and insurance planning, estate freezes can go wrong. Shares that fail the QSBC tests at the critical moment, crystallizations that trigger unexpected AMT, purifications that start too late, and trust structures that don’t account for the holding period — these are all mistakes we see in practice. In the next article, we walk through the most common estate freeze errors and how to avoid them.

For definitions of the key terms used in this article — including LCGE, QSBC shares, crystallization, AMT, and capital gains exemption — see our Key Terms and Definitions reference guide.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Estate freezes are complex transactions that require the coordinated involvement of qualified tax, valuation, and legal professionals. Always consult your advisors before acting on any of the information discussed here.