A shareholder agreement is as essential as the trust deed in an estate freeze. It governs what happens when a shareholder dies, divorces, becomes disabled, or wants out. Draft it at the time of the freeze, not after a dispute forces the conversation. Include a current valuation formula, funded buyout provisions, and dispute resolution mechanisms.

An estate freeze changes the ownership structure of your corporation. Where you were once the sole shareholder, there are now multiple shareholders — you (with preferred shares) and your successors or a family trust (with common shares). That new multi-shareholder reality creates the need for a document that governs the relationship between everyone at the table: a shareholder agreement.

In our practice, we won’t complete a freeze without one. A well-drafted shareholder agreement is just as important as the trust deed. Without it, the shareholders have no formal framework for handling the situations that inevitably come up — what happens if a shareholder wants to sell, if a shareholder dies, if a shareholder goes through a divorce, or if the shareholders simply disagree about where the business is headed.

Why a Shareholder Agreement Is Essential After a Freeze

What makes shareholder agreements especially important in estate freezes is that the parties are typically not at arm’s length. Family dynamics, emotional attachments to the business, and differing expectations about the future all push in the same direction once a trigger event arrives — toward conflict. The shareholder agreement is the document that was negotiated when everyone was thinking clearly, and it becomes the reference point when they aren’t.

There’s also a practical tax reason. When the freezor dies, subsection 70(5) of the Income Tax Act deems a disposition of the preferred shares at fair market value — triggering a capital gains tax liability on the estate. If the shareholder agreement doesn’t address how the shares are dealt with on death, the estate may face a tax bill with no mechanism to fund it, no obligation on the surviving shareholders to purchase the shares, and no agreed-upon price. The buy-sell provisions in a shareholder agreement solve all three problems.

What Happens Without a Shareholder Agreement

Let’s walk through what happens when there’s no agreement in place. A father freezes his manufacturing company and transfers growth shares to a family trust for his two children, Sarah and Michael. The father dies unexpectedly. Sarah has been running the business for ten years. Michael lives in another province and has no involvement in the company.

Without a shareholder agreement, there is no buy-sell mechanism, no agreed price for the preferred shares, and no obligation on either party to do anything. Michael, through the trust, now holds an indirect interest in the growth shares. He wants the trust to receive dividends. Sarah wants to reinvest in the business. There is no dispute resolution clause — their only option is the courts.

The father’s estate owes approximately $401,000 in capital gains tax on the deemed disposition of the preferred shares under subsection 70(5), but there’s no life insurance and no mechanism to redeem the shares. Eighteen months and $180,000 in combined legal fees later, the court orders the corporation to redeem the shares at a judicially determined price — which neither party is happy with. During the litigation, two key employees leave, a major contract is lost, and the business value drops by roughly 15%. We’ve seen variations of this scenario play out, and the damage is always worse than people expect.

In the scenario above, the total cost of not having a shareholder agreement — legal fees, lost business value, tax inefficiency, and family conflict — easily exceeds $500,000. A shareholder agreement drafted at the time of the freeze would have cost $5,000–$15,000 and prevented all of it.

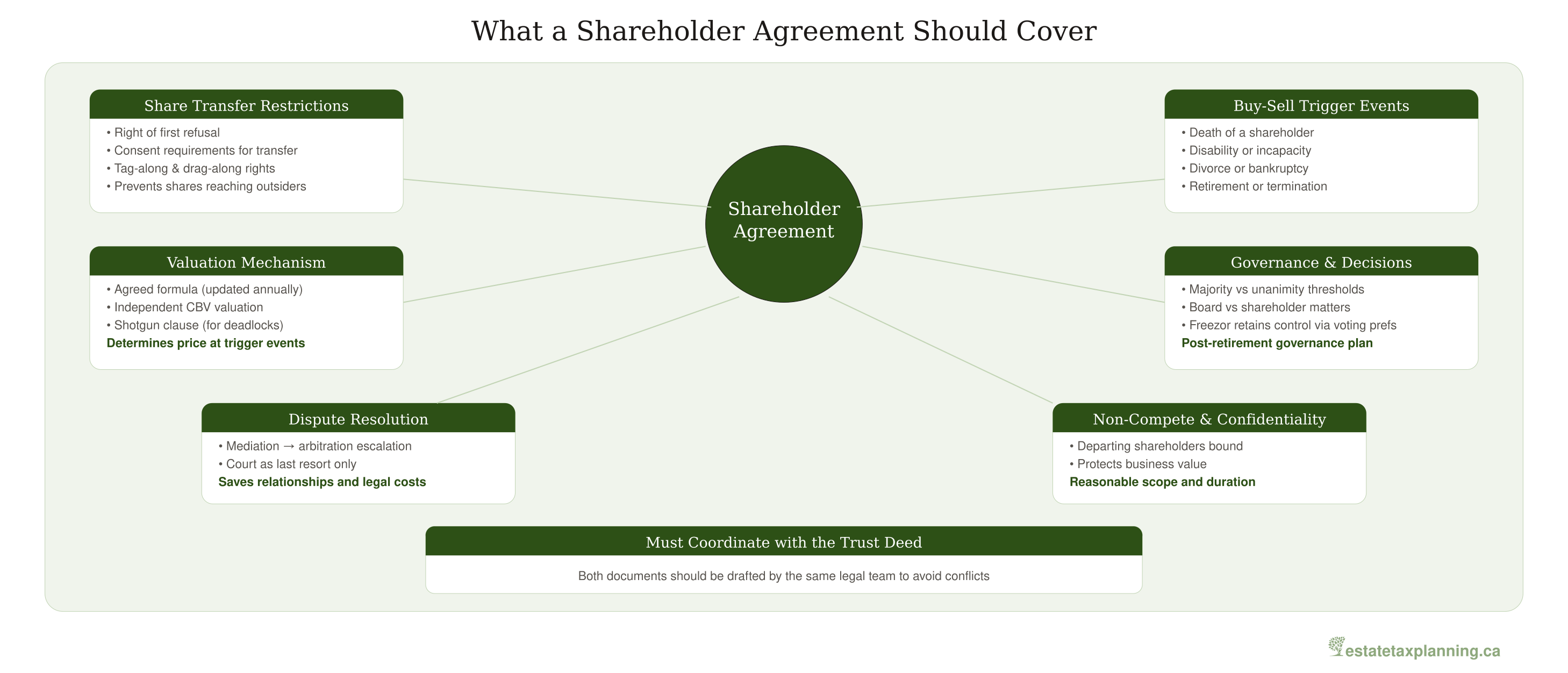

What a Shareholder Agreement Should Cover

Share Transfer Restrictions

Right of first refusal. If a shareholder wants to sell their shares, the other shareholders (or the corporation) have the first opportunity to purchase them at the same price. This prevents shares from ending up in the hands of outsiders without the consent of the remaining shareholders.

The agreement should specify that shares cannot be sold, transferred, pledged, or otherwise disposed of without the consent of the other shareholders (or the trustee, if a trust is involved). This is particularly important for growth shares — you do not want your child’s shares ending up with an ex-spouse or a creditor.

Tag-along and drag-along rights round out the transfer provisions. Tag-along rights protect minority shareholders by allowing them to participate in a sale if a majority shareholder sells. Drag-along rights allow a majority shareholder to compel minority shareholders to sell if a buyer wants 100% of the company. Both are important in a freeze context where ownership may be split unevenly.

Unanimous Shareholder Agreements

There is an important distinction between a regular shareholder agreement and a unanimous shareholder agreement (USA). A regular shareholder agreement is a contract among the shareholders that governs their relationship. A USA goes further — it can restrict or transfer the powers of the board of directors to the shareholders themselves. Under the Canada Business Corporations Act (subsection 146(1)) and the Ontario Business Corporations Act (section 108), a USA must be signed by all shareholders and can grant shareholders direct control over decisions that would otherwise belong to the board.

In an estate freeze context, a USA is often the better choice. When a family trust holds the growth common shares, the USA allows the trustee to participate directly in governance decisions — vetoing major capital expenditures, related-party transactions, or changes to the share structure — rather than relying solely on contractual rights. The trade-off is that a USA must be disclosed to new shareholders and can restrict the board’s ability to act quickly. For most family-owned businesses going through a freeze, that trade-off is worthwhile.

- A regular shareholder agreement is just a contract among the people who sign it. A USA actually binds the corporation and restricts what the directors are allowed to decide. That is a bigger distinction than most clients realize on first read.

- Every shareholder has to sign a USA — including the family trust, through its trustees. New shareholders have to be given notice of it before they buy in.

- When a family trust holds the growth shares, a USA gives the trustees real governance teeth rather than just contractual remedies. For freeze structures, that is our default recommendation.

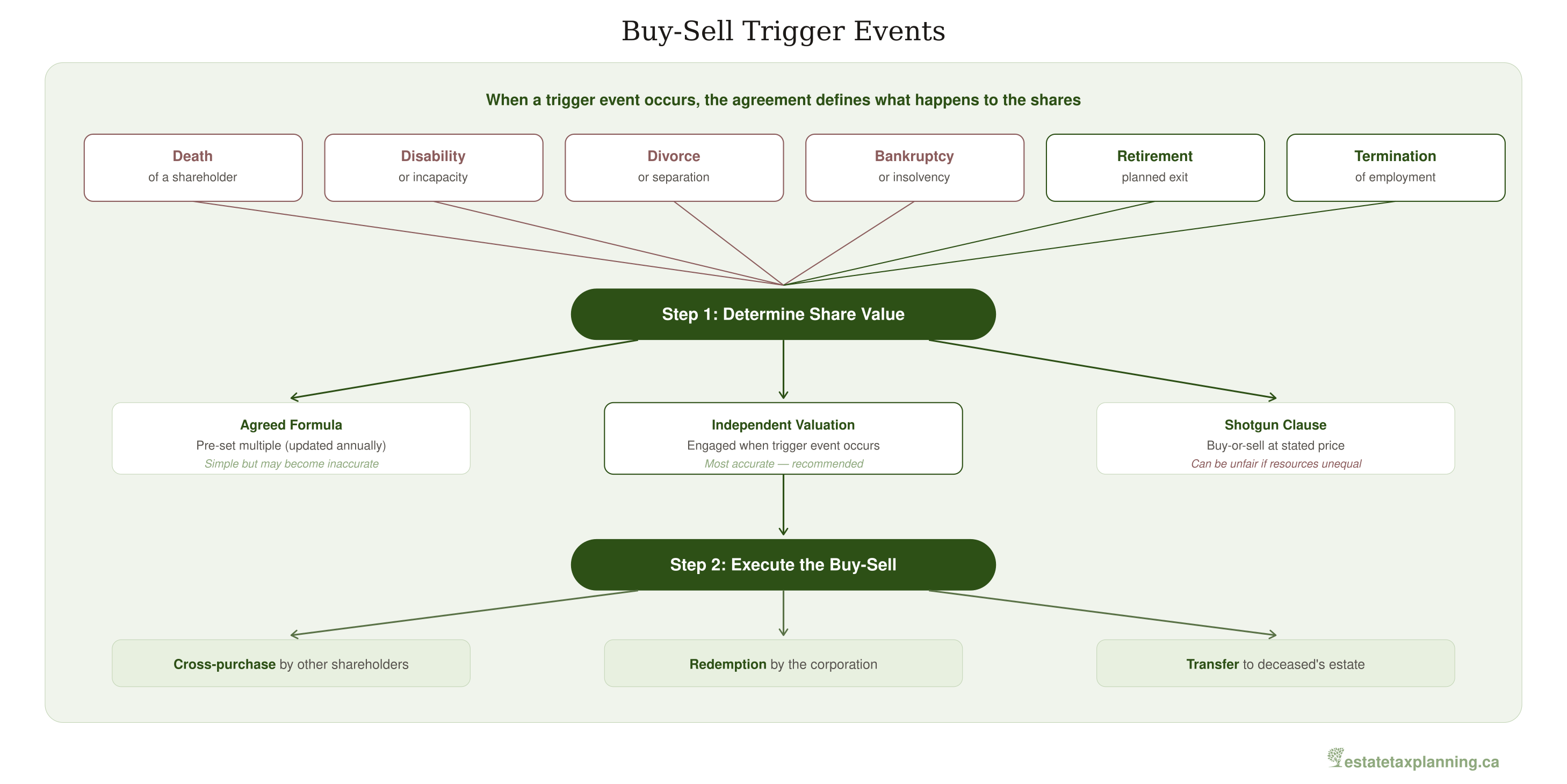

Buy-Sell Provisions (Trigger Events)

The trigger events are the heart of the agreement — they are what the document is really for. In a freeze context we plan around six of them, and each one has its own tax consequences, its own funding problem, and its own failure mode when the agreement is silent.

| Trigger Event | What Happens | Key Considerations |

|---|---|---|

| Death of a shareholder | Shares are purchased by surviving shareholders, redeemed by the corporation, or transferred to the estate | Life insurance typically funds this purchase; see Life Insurance and the Estate Freeze |

| Disability or incapacity | Shares are dealt with after a defined waiting period (often 6–12 months of continuous disability) | Define “disability” precisely and align it with the insurance policy definition; see Incapacity and Disability Planning |

| Retirement | Preferred shares are redeemed on a schedule (the wasting freeze) | Particularly relevant for the freezor; the agreement defines the redemption timeline and annual limits |

| Divorce or separation | Provisions prevent shares from being transferred to an ex-spouse as matrimonial property | Coordinate with a domestic contract; see Protecting Estate Freeze Shares from Divorce |

| Bankruptcy or insolvency | Shares must be offered for sale to other shareholders before creditors can seize them | The agreement should require immediate notice and a short exercise window (e.g., 30 days) |

| Termination of employment | Departing employee-shareholders must sell their shares at the agreed price | Distinguish between voluntary resignation, termination with cause, and termination without cause |

Tax Implications of Buy-Sell Provisions

You can’t draft effective buy-sell provisions without understanding the tax consequences of each trigger event. The most significant is death. Under subsection 70(5) of the Income Tax Act, when a shareholder dies, their shares are deemed to have been disposed of at fair market value immediately before death. This triggers a capital gain on the difference between the FMV and the adjusted cost base (ACB) of the shares — and the resulting tax is payable by the deceased’s estate.

Let’s put numbers to it. A freezor holds preferred shares with a fair market value of $2,000,000 and an adjusted cost base of $500,000. (In this example, the ACB reflects a prior LCGE crystallization at the time of the freeze — in many cases the ACB will be nominal, which makes the capital gain even larger.) On death, subsection 70(5) deems a disposition at FMV, creating a capital gain of $1,500,000. At a 50% inclusion rate, the taxable capital gain is $750,000. At Ontario’s top combined marginal rate of approximately 53.53%, the tax on this gain is approximately $401,000. Without a funded buy-sell agreement, the estate has to come up with $401,000 in cash — potentially forcing a fire sale of the business or its assets.

How Insurance Funds the Buy-Sell: A Complete Example

Continuing the example above, suppose the corporation owns a $2,000,000 life insurance policy on the freezor’s life, with an adjusted cost basis (ACB) of $100,000. When the freezor dies, the corporation receives the $2,000,000 death benefit tax-free. Here is how the numbers flow through the buy-sell:

The excess of the death benefit over the policy’s ACB — $2,000,000 minus $100,000, or $1,900,000 — is credited to the corporation’s Capital Dividend Account (CDA). The corporation then redeems the deceased freezor’s preferred shares for $2,000,000. Under subsection 84(3), the portion of the redemption amount that exceeds the shares’ paid-up capital (PUC) is treated as a deemed dividend. If the PUC is $500,000, the deemed dividend is $1,500,000.

By electing to pay a capital dividend from the CDA, the corporation designates $1,500,000 of the redemption amount as a capital dividend — which the estate receives entirely tax-free. The remaining $500,000 is a return of PUC, also tax-free. The estate receives the full $2,000,000 and pays no tax on the redemption itself. The estate still owes approximately $401,000 from the subsection 70(5) deemed disposition, but the net result is roughly $1,600,000 retained — all funded by the insurance policy.

- With a funded buy-sell: The estate receives $2,000,000, pays ~$401,000 in tax, and retains ~$1,600,000. The business continues operating without interruption.

- Without a funded buy-sell: The estate owes ~$401,000 with no immediate source of cash. The preferred shares are illiquid. The estate may need to petition the court, incurring $100,000+ in legal fees over 12–18 months while the business deteriorates. We’ve seen this scenario play out — it’s devastating for the family and the business.

- The annual insurance premium — typically $5,000–$15,000 for a $2,000,000 term policy — is a fraction of the cost of not having coverage. It’s the most cost-effective piece of the entire freeze structure.

On a redemption, subsection 84(3) turns the excess of the redemption amount over PUC into a deemed dividend — not a capital gain — taxed at the estate’s marginal rate (up to 39.34% eligible or 47.74% non-eligible in Ontario). The estate may also realize a capital loss on the shares, and the interaction between the CDA election, the deemed dividend, and that capital loss is where we see files go sideways. The mechanics work only if the CPA and the lawyer are on the same email thread before the redemption happens, not after.

Insurance Funding Structures

Three funding structures tend to show up in practice — corporate-owned (entity redemption), cross-purchase, and criss-cross (trustee-held). They differ in who pays the premiums, who gets the CDA credit, and how flexible the structure is when the shareholder mix changes. The table below compares them at a glance; for the full mechanics, see Life Insurance and the Estate Freeze and Life Insurance Tax Mechanics.

| Structure | Policy Owner | Premium Source | Tax Treatment of Proceeds |

|---|---|---|---|

| Corporate-owned (entity redemption) | Corporation | Corporate funds (pre-tax equivalent) | Death benefit excess over ACB credited to CDA; enables tax-free capital dividends |

| Cross-purchase | Each shareholder owns policy on others | Personal after-tax dollars | Surviving shareholder gets stepped-up ACB on purchased shares; no CDA credit |

| Criss-cross (trustee) | Independent trustee holds policies on each shareholder | Typically corporate funds | At death, trustee directs proceeds to whichever structure (redemption or cross-purchase) is most tax-efficient given the CDA balance and shareholder mix at that time |

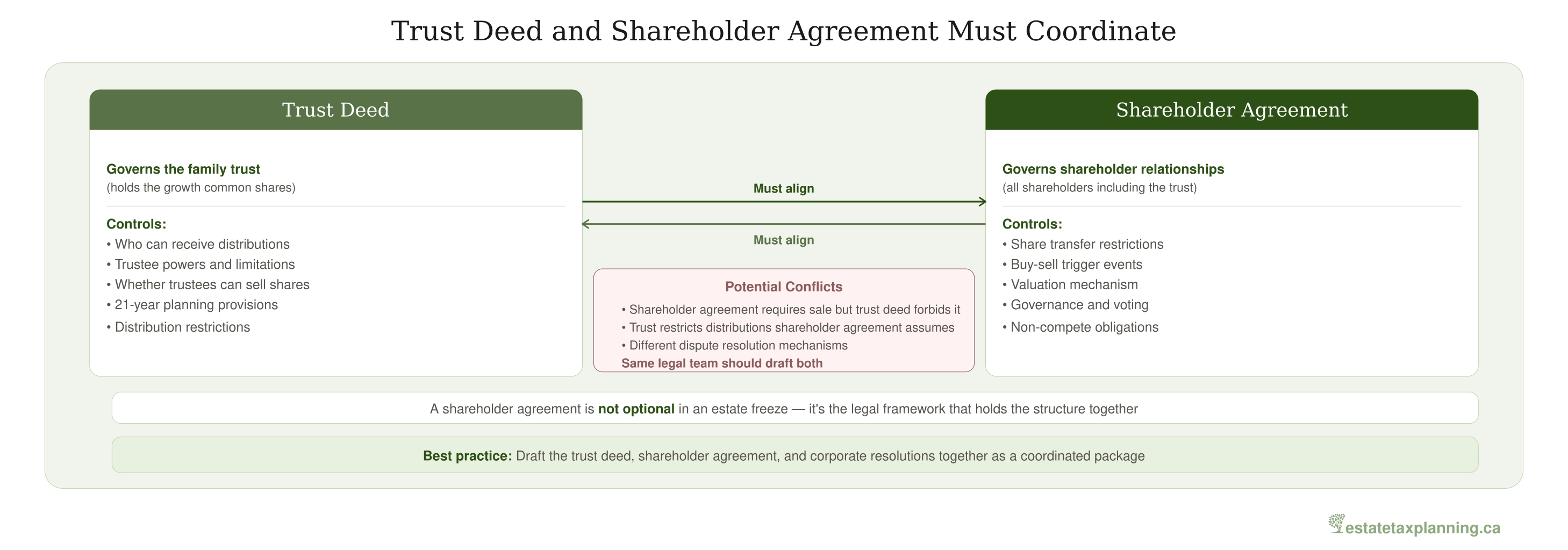

Coordination with the Trust Deed

A shareholder agreement doesn’t stand alone — and this is a point we emphasize with every client. If a family trust holds the growth shares, the shareholder agreement and the trust deed must work in concert. The trust deed governs how the trustees manage the trust’s shares, while the shareholder agreement governs the relationship between all shareholders (including the trust). These documents should be drafted by the same legal team to avoid conflicts.

For example, if the shareholder agreement requires that a deceased shareholder’s shares be offered to the corporation at the agreed formula price, the trust deed must authorize the trustees to accept that price — even if it is below the current FMV. If the trust deed restricts distributions but the shareholder agreement assumes the trust can participate in a cross-purchase, the two documents conflict. The dispute resolution mechanism in the shareholder agreement should also align with any dispute resolution provisions in the trust deed.

The most frequent problems we see in shareholder agreements after an estate freeze are: (1) the agreed formula has not been updated in years, creating a price that no longer reflects the business value; (2) the trust deed and shareholder agreement were drafted by different lawyers and contain conflicting provisions; (3) the life insurance coverage has not kept pace with the growth in share value, leaving a funding gap; and (4) the agreement does not address what happens to the freeze shares when the 21-year deemed disposition rule applies to the family trust.

Valuation, Governance, and Other Key Provisions

Valuation Mechanism

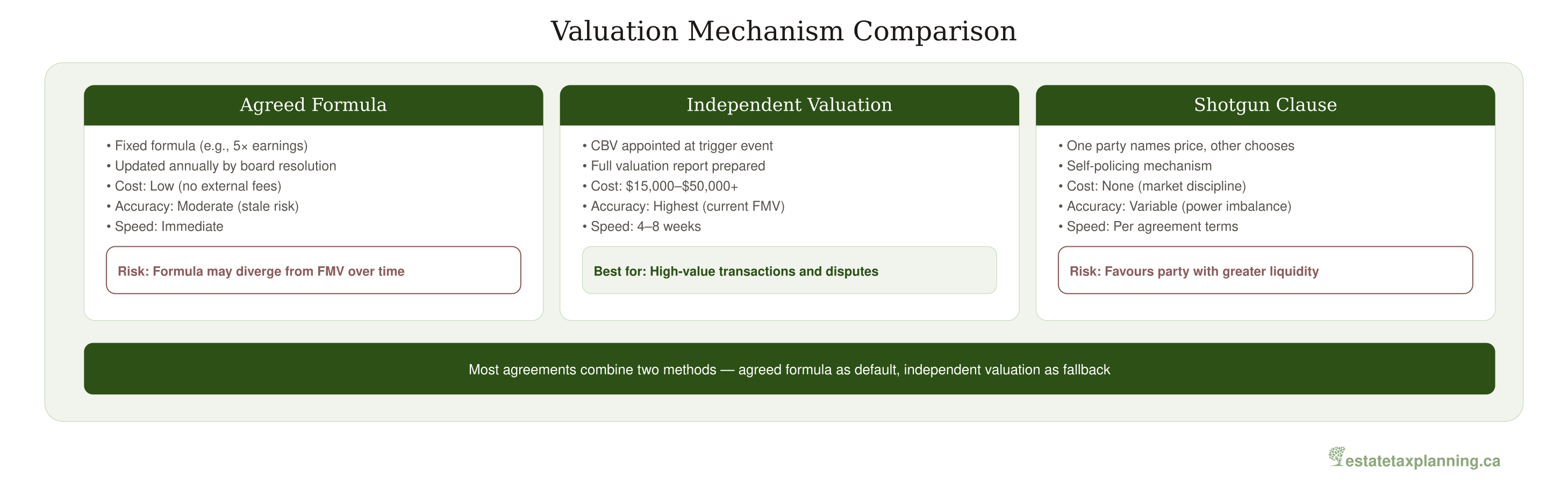

Getting the valuation mechanism wrong is, in our experience, just as damaging as not having a buy-sell clause at all — a stale formula or an undefined process is usually what turns an otherwise routine trigger event into a years-long dispute. Three approaches come up again and again, each with different cost and accuracy trade-offs.

| Mechanism | How It Works | Advantages | Disadvantages |

|---|---|---|---|

| Agreed formula | Shareholders agree on a formula (e.g., 5× normalized earnings or book value plus goodwill premium) updated annually by board resolution | Low cost, immediate price determination, no external fees | Becomes stale if not updated annually; may diverge significantly from true FMV over time |

| Independent CBV valuation | A Chartered Business Valuator is engaged when a trigger event occurs to prepare a full valuation report determining FMV | Most accurate reflection of current FMV; defensible for CRA purposes; cost of $15,000–$50,000+ | Takes 4–8 weeks; expensive; may create delay in time-sensitive situations (e.g., death) |

| Shotgun clause | One shareholder offers to buy the other’s shares at a stated price; the other must accept the offer or buy the first shareholder’s shares at that same price | Self-policing (the offeror must name a fair price); effective for deadlock resolution | Can be unfair when shareholders have significantly different financial resources; not appropriate for family freeze situations with parents and children |

Most well-drafted agreements combine two methods — an agreed formula as the default, updated annually by the board, with an independent CBV valuation as a fallback if either party disputes the formula price. The shotgun clause is typically reserved for unresolvable deadlocks between arm’s-length shareholders and is less common in family freeze situations where the parties have unequal financial resources.

- We’ve seen shareholder agreements where the “agreed value” hasn’t been updated in eight years. When a trigger event finally happens, the buyout price bears no resemblance to what the business is actually worth — and that’s when the lawsuits start.

- A simple board resolution confirming the formula value each year takes less than an hour and costs nothing — but failing to do it can cost hundreds of thousands of dollars if a trigger event occurs with an outdated valuation. We calendar this for every client.

- Some agreements include an automatic escalator (e.g., the last agreed value increases by CPI annually until the next board update) as a safety net against stale valuations. We recommend this as a backstop, but it’s no substitute for an annual review.

When a buy-sell triggers between non-arm’s-length parties, CRA may challenge the transaction if the agreed price differs significantly from FMV. Three practices help: update the formula annually and document the board resolution, include a price adjustment clause that allows retroactive adjustment if CRA determines a different FMV, and for businesses with shares worth over $1,000,000, obtain a periodic independent CBV valuation every three to five years as a defensible benchmark.

Dispute Resolution

The single most valuable clause in the agreement is often the one that keeps the parties out of court. Build in a defined escalation path — good-faith negotiation for a fixed window (we typically use 30 days), then formal mediation with a neutral third party, then binding arbitration if mediation fails. Litigation between family members who are also business partners destroys the family relationship and the enterprise value at the same time, and it is almost always the worst available option.

The cost differential is significant. Mediation typically costs $5,000–$15,000 and resolves within weeks. Arbitration costs $20,000–$50,000 and takes a few months. Litigation can exceed $100,000 per party and drag on for years. The agreement should specify the rules governing each stage — for example, that arbitration will be conducted by a single arbitrator with corporate valuation experience and that the decision is final and binding.

Non-Competition and Confidentiality

Shareholders who leave the business should be bound by reasonable non-competition and confidentiality obligations. Canadian courts will enforce non-competition clauses only if they are reasonable in scope, geography, and duration — typically two to five years within a defined area. Enforceability varies by province — consult your corporate lawyer on the specific restrictions that are supportable in your jurisdiction. Overly broad restrictions will be struck down entirely. Confidentiality obligations are typically broader and longer-lasting: the agreement should define what constitutes confidential information and prohibit its use or disclosure indefinitely.

Governance and Decision-Making

The agreement should define how major decisions are made — what requires a simple majority, what requires a supermajority (e.g., 75%), and what requires unanimity. In a freeze context, the freezor typically retains control through voting preferred shares, but the agreement also needs to address how decisions are made after the freezor’s death or retirement. That transition period is where we see the most governance disputes. Common supermajority items include the issuance of new shares, the sale of substantially all assets, changes to the articles of incorporation, and related-party transactions.

The agreement should also address board composition. Can the freezor always appoint a majority of the directors? After the freezor’s death, does the trust (holding the growth common shares) have the right to appoint one or more directors? These governance provisions become critical during the transition from one generation to the next — the period when the freeze structure is most vulnerable to internal conflict.

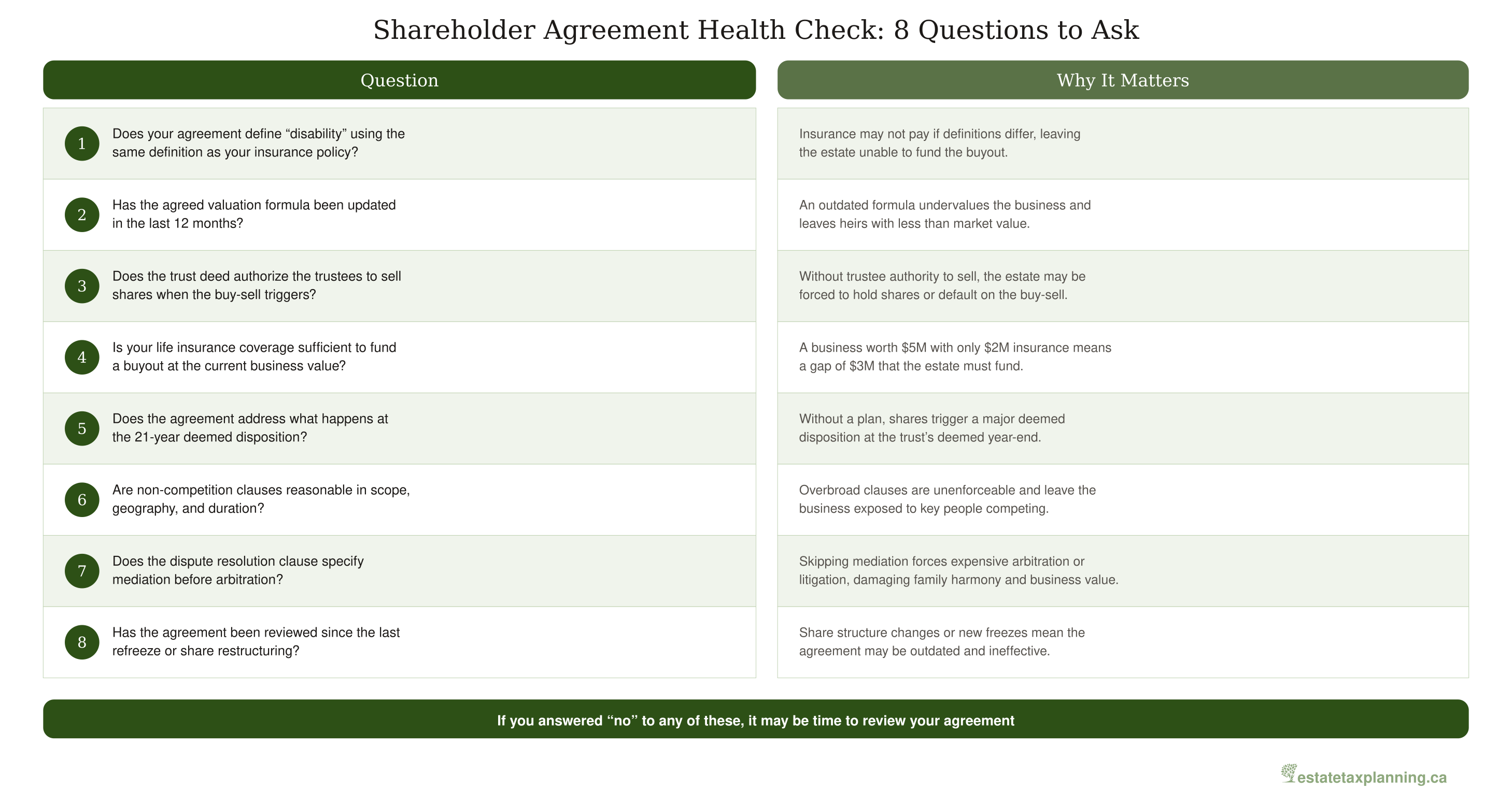

Shareholder Agreement Health Check

These are the eight questions we work through with clients on every shareholder agreement review — whether we are drafting a new one alongside a freeze or auditing one that has been sitting in the corporate minute book for a decade. A “no” to any of them is the signal to call your legal and tax advisors.

Plan on a formal review at least every three years — sooner if there is a refreeze, a change in the shareholder group, a material jump in business value, or a change in insurance coverage. A shareholder agreement is not a “set it and forget it” document, and the files we open most often in crisis mode are the ones nobody has read since the freeze closed.

- It provides a neutral framework for handling shareholder disputes before emotions escalate — mediation first, litigation last.

- It prevents shares from ending up in the hands of unintended parties through transfer restrictions and buy-sell trigger events.

- It defines clear valuation mechanisms and insurance funding structures so that when a trigger event occurs, the price and the money are both ready.

- It coordinates with the trust deed to ensure the legal documents work together, not against each other.

What’s Next

If you already have a shareholder agreement, take the time to review it with your legal and tax advisors using the eight questions above. If you don’t have one, commissioning a shareholder agreement at the same time as the freeze — typically $5,000–$15,000 — is one of the most cost-effective investments you can make to protect the structure. It’s a fraction of what the litigation costs when things go wrong.

In the next article, Protecting Estate Freeze Shares from Divorce, we explore how family law intersects with your freeze structure — including domestic contracts, matrimonial property division, and the provisions your shareholder agreement needs to address the risk of a shareholder’s marriage breakdown.

For more on the topics discussed in this article, see Life Insurance and the Estate Freeze (how insurance funds the tax liability), Incapacity and Disability Planning (disability triggers and insurance alignment), and Trust Governance (family councils, advisory boards, and next-generation governance).

For definitions of the key terms used in this article — including shareholder agreement, buy-sell provision, deemed dividend, capital dividend account, and unanimous shareholder agreement — see our Key Terms and Definitions reference guide.

Your tax advisor, CBV, and legal counsel can help you evaluate how this applies to your situation — a shareholder agreement drafted alongside the freeze, with a current valuation formula, funded buy-sell provisions, and a coordinated trust deed, is typically a small fraction of the cost of the litigation it is designed to prevent.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Estate freezes are complex transactions that require the coordinated involvement of qualified tax, valuation, and legal professionals. Always consult your advisors before acting on any of the information discussed here.